Renovation Spending Gains Ground as New Construction Shifts by Sector and Region Q1 2026

Residential renovation work took on a larger role in the first quarter of 2026, while new construction continued to carry several major categories. The national figures show a construction sector moving unevenly, with different pressures in single-family housing, multi-unit residential work, commercial buildings and institutional projects.

Residential renovation work took on a larger role in the first quarter of 2026, while new construction continued to carry several major categories. The national figures show a construction sector moving unevenly, with different pressures in single-family housing, multi-unit residential work, commercial buildings and institutional projects.

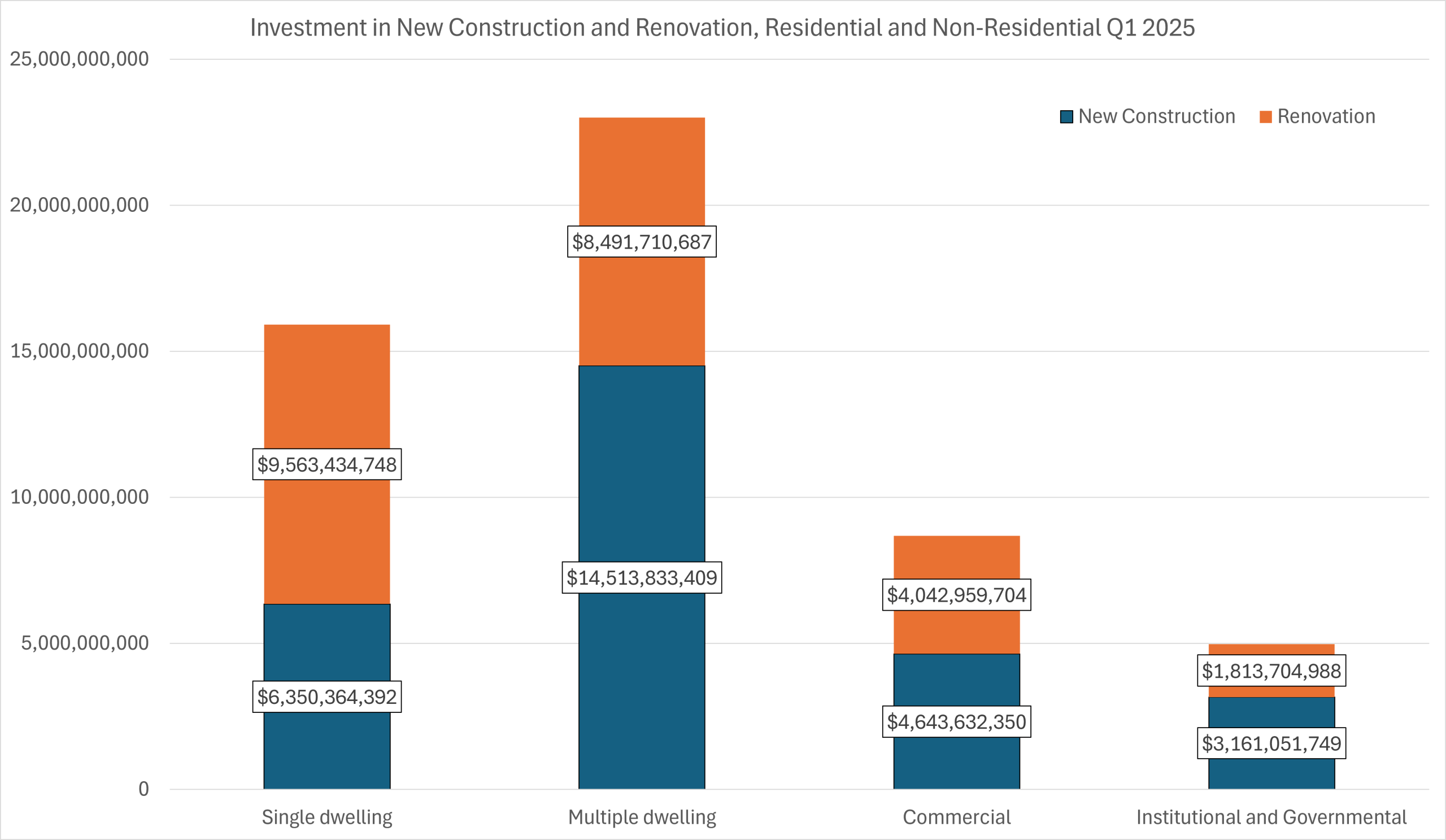

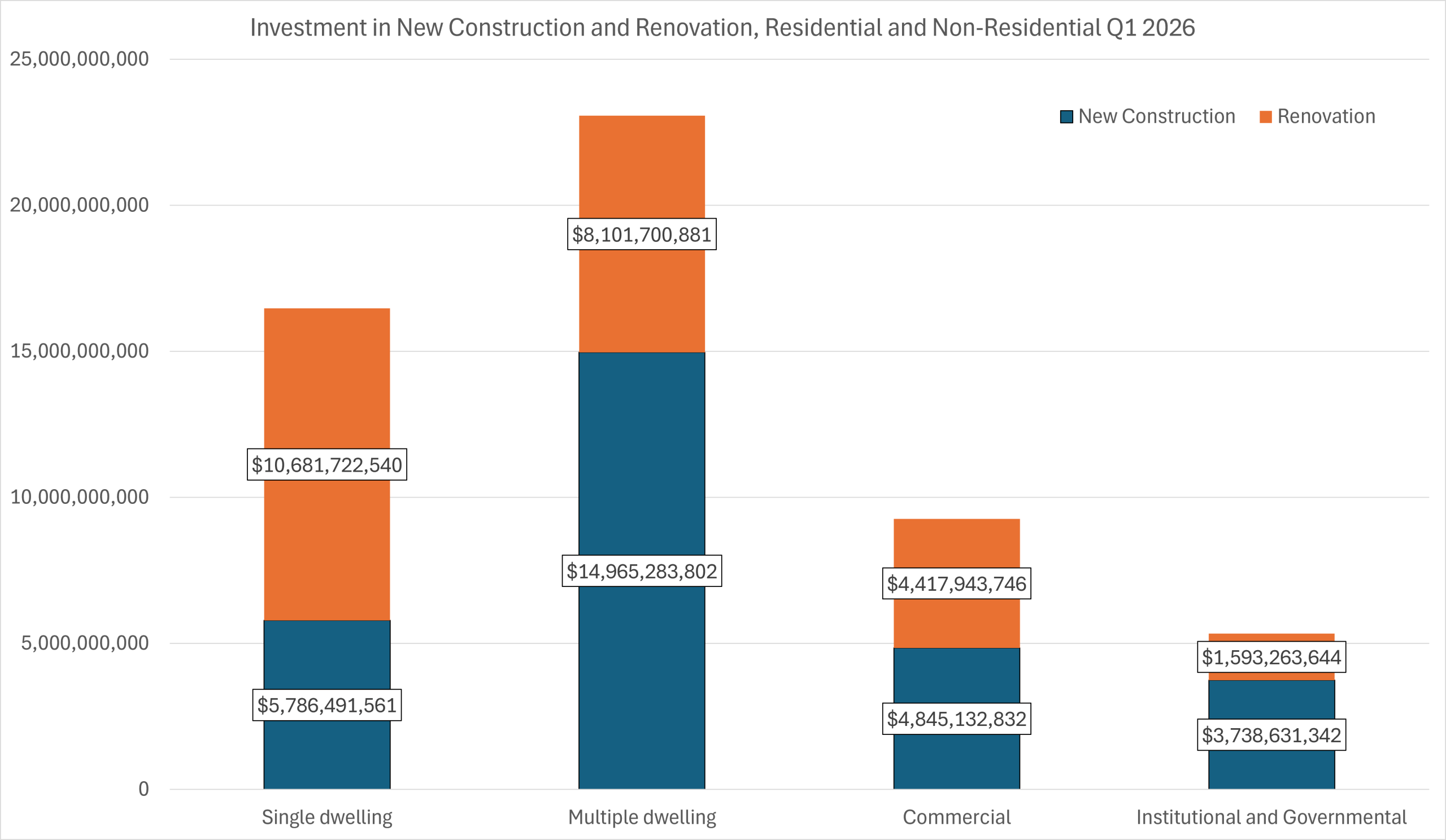

Investment in single-dwelling new construction fell from $6.35 billion in Q1 2025 to $5.79 billion in Q1 2026, a decline of about 8.9 per cent.  Renovation spending in the same category moved the other way, rising from $9.56 billion to $10.68 billion, up roughly 11.7 per cent. Fewer dollars are going into new single-dwelling construction, while more are being directed into existing homes.

Renovation spending in the same category moved the other way, rising from $9.56 billion to $10.68 billion, up roughly 11.7 per cent. Fewer dollars are going into new single-dwelling construction, while more are being directed into existing homes.

On job sites, the work is different. New single-family construction usually follows a more linear sequence, from site work and framing through rough-ins, finishing and handover. Renovation work is less predictable. Crews are often dealing with occupied homes, older building systems, partial demolition, hidden deficiencies and customer decisions made after work has started. The increase favours firms that can manage uncertainty without losing control of scheduling or margin.

Multi-dwelling construction remains the largest national new-build category in the dataset. Spending on new multiple dwellings increased from $14.51 billion in Q1 2025 to $14.97 billion in Q1 2026, up about 3.1 per cent. Renovation spending in the category declined from $8.49 billion to $8.10 billion, down about 4.6 per cent.

Apartments, condominiums and other multi-residential projects continue to drive residential new construction spending. These projects carry long planning cycles, larger financing commitments and more complicated procurement than single-family builds. A modest national increase does not mean conditions have become easier for builders. It does show that multi-unit projects continued to absorb substantial capital in early 2026.

Commercial construction was more balanced. New commercial construction rose from $4.64 billion to $4.85 billion, an increase of about 4.3 per cent. Commercial renovation spending increased faster, from $4.04 billion to $4.42 billion, up about 9.3 per cent. The gap between new and renovation spending narrowed.

That movement often shows up in tenant improvements, building upgrades, interior reconfigurations and repositioning projects. Owners may be investing in existing space rather than committing entirely to new buildings. For mechanical, electrical, flooring, millwork, glazing and interior finishing trades, renovation activity can keep work moving even when larger new-build decisions are more selective.

Institutional and governmental construction showed the strongest national increase in new construction. Spending rose from $3.16 billion in Q1 2025 to $3.74 billion in Q1 2026, an increase of about 18.3 per cent. Renovation spending in the same sector declined from $1.81 billion to $1.59 billion, down about 12.2 per cent.

Capital appears to be moving more heavily into new institutional projects than into upgrades of existing public-sector buildings. Institutional work usually comes with formal procurement, longer design periods, tighter documentation requirements and layered approvals. Contractors in that market are often managing compliance and sequencing as much as the physical work.

The provincial and regional data shows the unevenness beneath the national totals.

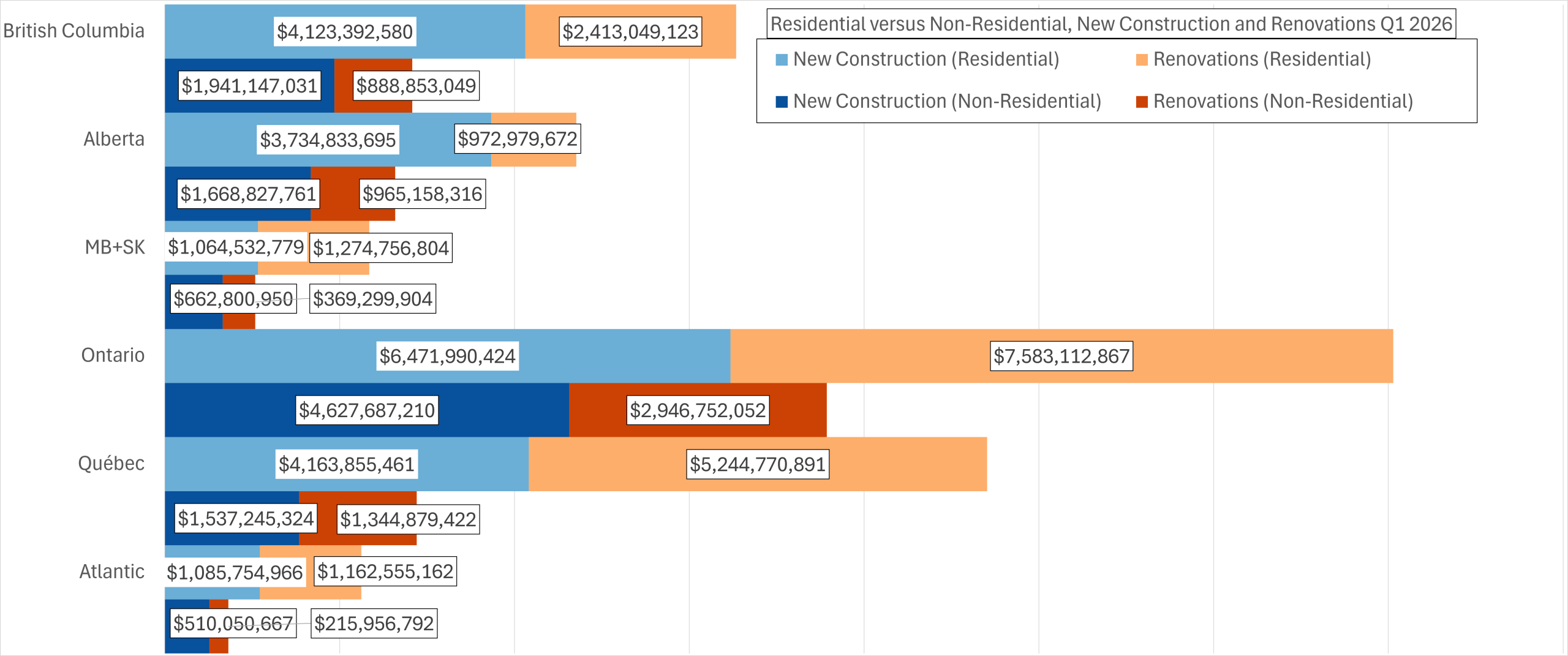

Ontario remains the largest market in the dataset, but its residential numbers weakened. Residential new construction fell from $7.67 billion in Q1 2025 to $6.47 billion in Q1 2026. Residential renovation spending also declined, from $8.28 billion to $7.58 billion. Even after those declines, Ontario still posted the largest residential renovation total among the provinces and regions shown. Its non-residential figures were steadier. New non-residential construction increased slightly from $4.59 billion to $4.63 billion, while non-residential renovation edged up from $2.94 billion to $2.95 billion.

For firms operating in Ontario, the data suggests residential softness rather than a broad construction pullback. Residential activity declined, while non-residential spending held close to the previous year’s level.

British Columbia posted growth in three of the four categories. Residential new construction increased from $3.82 billion to $4.12 billion. Residential renovation rose from $2.04 billion to $2.41 billion. Non-residential new construction increased from $1.71 billion to $1.94 billion. Non-residential renovation was essentially flat, slipping slightly from $891.7 million to $888.9 million.

The B.C. figures show a more active environment across new residential work and renovation. The renovation increase came alongside growth in new residential construction, not in place of it. That combination can put pressure on trades that serve both markets, including electrical, plumbing, HVAC, finishing and exterior envelope work.

Alberta’s numbers show a different split. Residential new construction rose from $3.44 billion to $3.73 billion, but residential renovation spending fell sharply from $1.61 billion to $973 million. Non-residential spending moved strongly upward. New non-residential construction increased from $1.32 billion to $1.67 billion, while non-residential renovation rose from $688 million to $965 million.

Québec moved differently. Residential new construction increased from $3.92 billion to $4.16 billion, while residential renovation rose more sharply, from $4.06 billion to $5.24 billion. Non-residential spending declined in both categories. New non-residential construction fell from $1.76 billion to $1.54 billion, and non-residential renovation declined from $1.62 billion to $1.34 billion.

Québec’s residential renovation total is one of the larger regional changes in the dataset. It exceeded residential new construction by more than $1 billion in Q1 2026. For suppliers and trades, that kind of renovation demand usually means more fragmented work, more customer-specific product selection and greater pressure on scheduling flexibility.

Manitoba and Saskatchewan, reported together, showed growth across all four categories. Residential new construction increased from $841 million to $1.06 billion. Residential renovation rose from $938 million to $1.27 billion. New non-residential construction moved from $627 million to $663 million, and non-residential renovation increased from $308 million to $369 million.

Atlantic Canada was mixed, but most categories increased. Residential new construction declined slightly from $1.12 billion to $1.09 billion. Residential renovation rose from $1.07 billion to $1.16 billion. New non-residential construction increased from $430 million to $510 million, while non-residential renovation rose from $190 million to $216 million.

The first-quarter figures show several adjustments rather than one national trend. Multi-unit residential remains the largest new-build category. Single-dwelling investment is shifting toward renovation. Commercial spending is rising on both new space and existing buildings. Institutional capital is moving more heavily into new construction.

For the industry, the implications are practical. Firms tied closely to single-family new builds are working in a softer national spending environment. Renovation-oriented contractors are seeing stronger demand, but with the jobsite complexity that comes with existing structures. Multi-residential builders remain tied to large projects with long schedules and financing exposure. Non-residential contractors face conditions that vary sharply by province.