Q4 2025 Building Investment Trends: Residential Strength Offsets Mixed Non-Residential Performance

Canada’s construction investment profile in Q4 2025 reflects a familiar but intensifying dynamic. Residential activity continues to carry overall growth, driven increasingly by renovations and multi-unit construction, while non-residential segments remain comparatively stable with pockets of softness. The shift is not uniform across categories or regions, but the direction is clear: capital is concentrating in areas tied to housing supply and adaptation of existing stock.

National Overview

National Overview

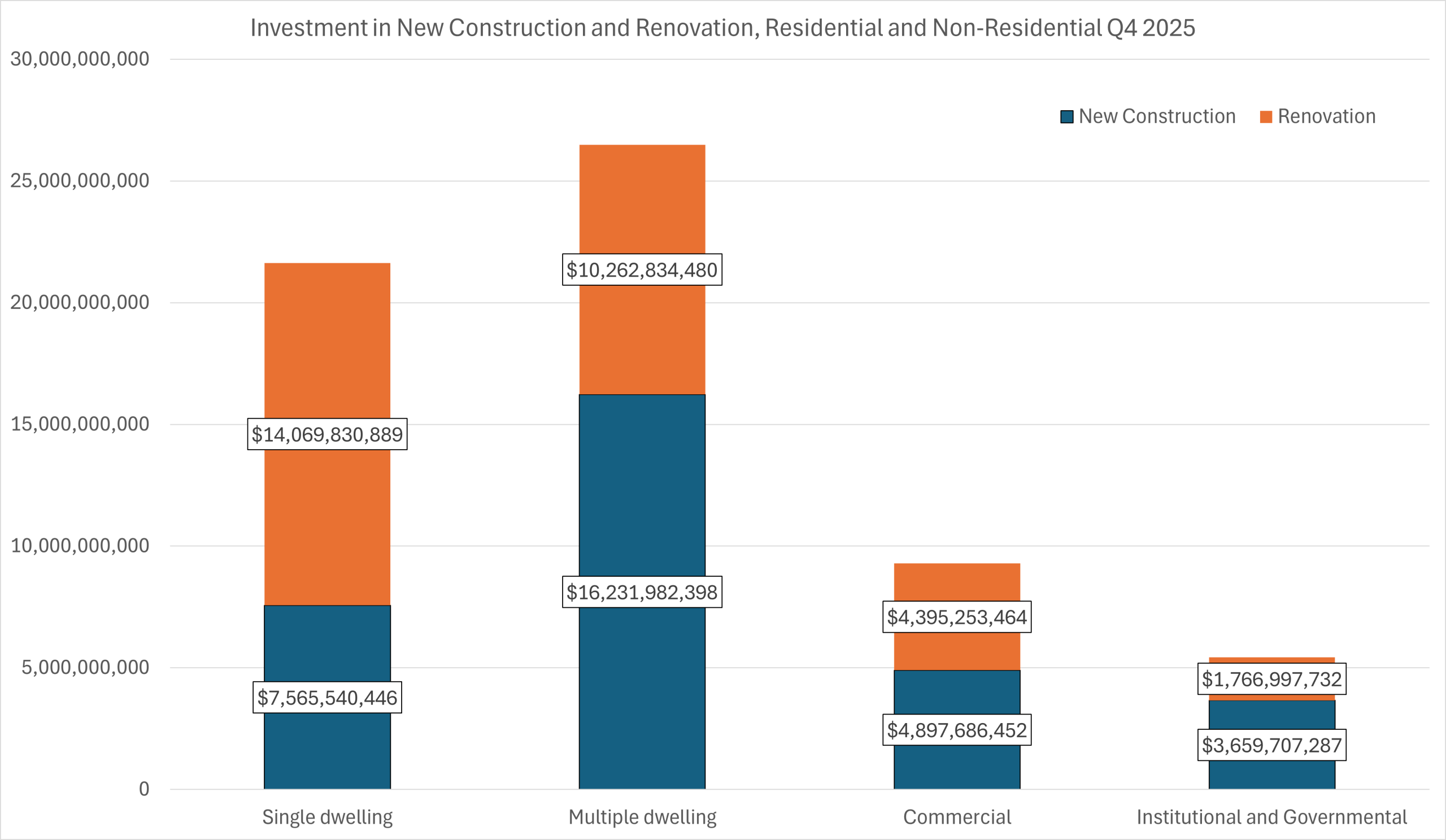

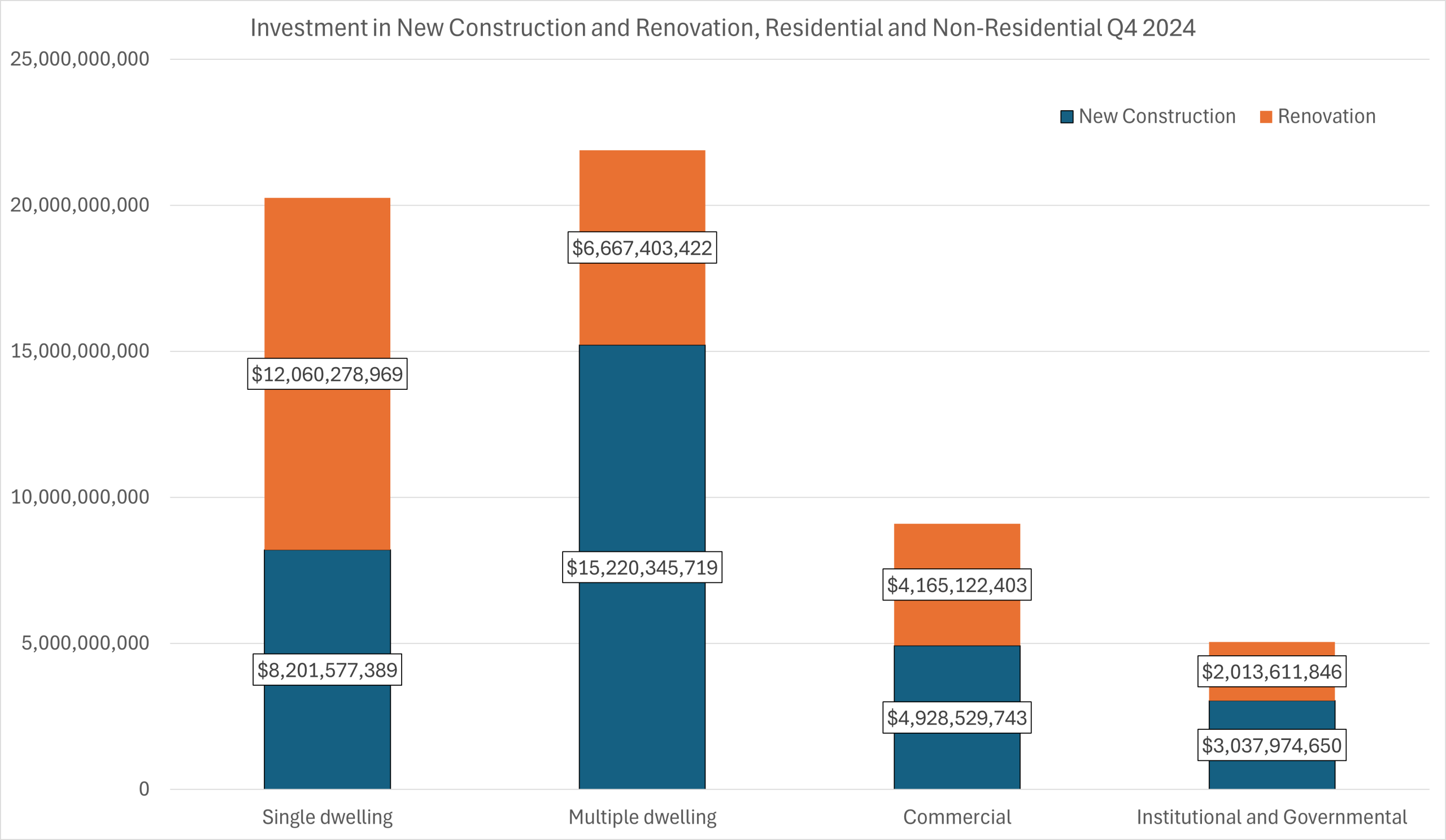

At the national level, construction investment in Q4 2025 shows clear growth on the residential side, while non-residential activity remains comparatively stable with more limited gains. Total residential investment increased from approximately $42.1 billion in Q4 2024 to $48.1 billion in Q4 2025, driven by both multi-unit construction and a sharp rise in renovation activity. Non-residential investment grew more modestly, from $14.1 billion to $14.7 billion, with different dynamics across commercial and institutional segments.

Within residential construction, the divergence between single and multi-dwelling activity is pronounced. Investment in new single dwelling construction declined from $8.2 billion to $7.6 billion, reflecting ongoing constraints in affordability, financing, and land availability. At the same time, renovation spending in this segment increased significantly, rising from $12.1 billion to $14.1 billion. This suggests that households are increasingly choosing to reinvest in existing properties rather than pursue new builds.

In contrast, the multi-dwelling segment continues to expand. New construction increased from $15.2 billion to $16.2 billion, indicating sustained demand for higher-density housing formats. Renovation activity in this segment also grew sharply, from $6.7 billion to $10.3 billion. This acceleration points to both reinvestment in existing multi-unit stock and adaptation of properties to meet evolving rental and urban housing demand. Taken together, residential growth is being driven less by low-density expansion and more by intensification and upgrading.

Within non-residential construction, the commercial segment remains the largest component but shows limited growth. New commercial construction edged down slightly from $4.93 billion to $4.90 billion, indicating a cautious approach to new project starts. However, renovation spending increased from $4.17 billion to $4.40 billion, suggesting continued investment in upgrading and repositioning existing commercial assets. This shift toward renovation reflects a preference for optimizing current space rather than expanding capacity in uncertain market conditions.

The institutional and governmental segment presents a different trajectory. New construction increased from $3.04 billion to $3.66 billion, signaling continued public-sector investment in infrastructure and major projects. In contrast, renovation spending declined from $2.01 billion to $1.77 billion. This indicates a tilt toward new builds over lifecycle upgrades, likely tied to project timing and funding cycles.

Overall, the national picture is defined by a strong residential sector driven by multi-unit growth and renovation activity, alongside a non-residential sector that is stable but uneven. Commercial activity is holding steady with a shift toward renovation, while institutional and governmental investment is supporting growth primarily through new construction.

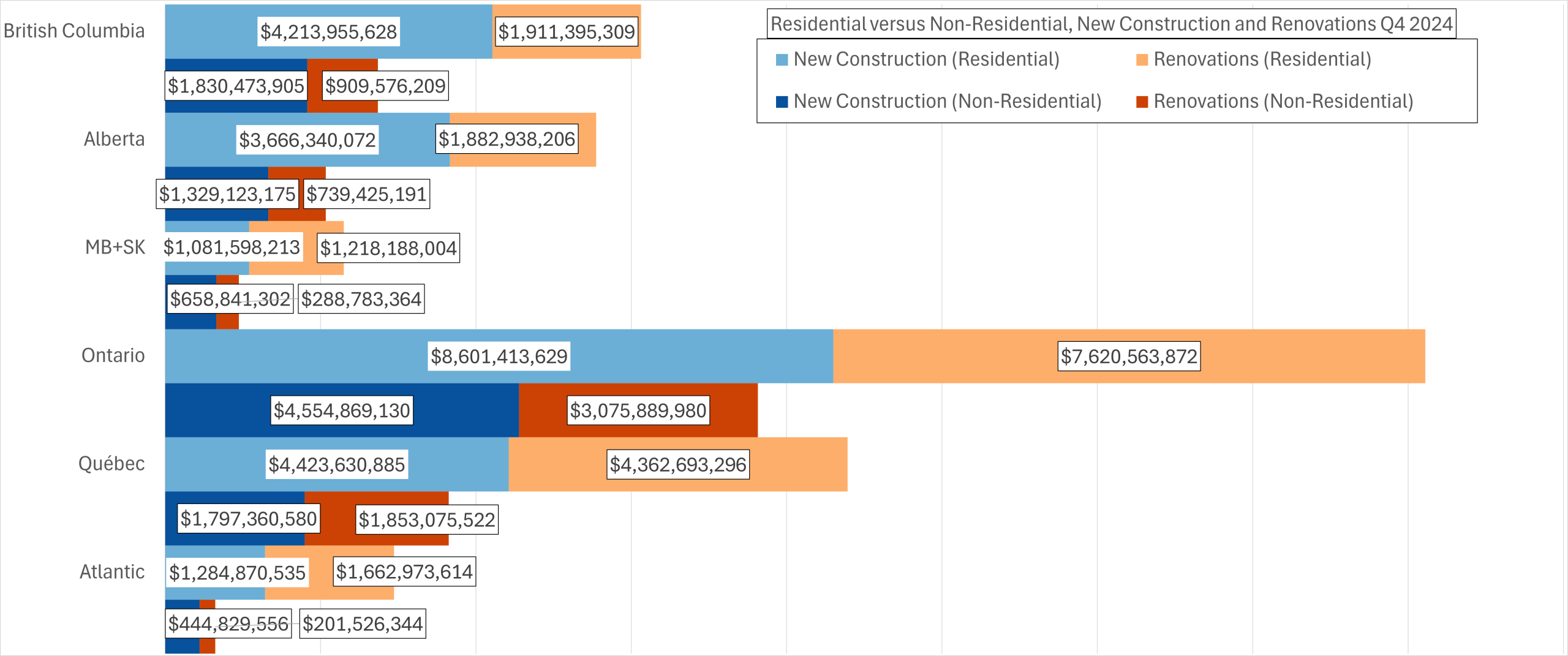

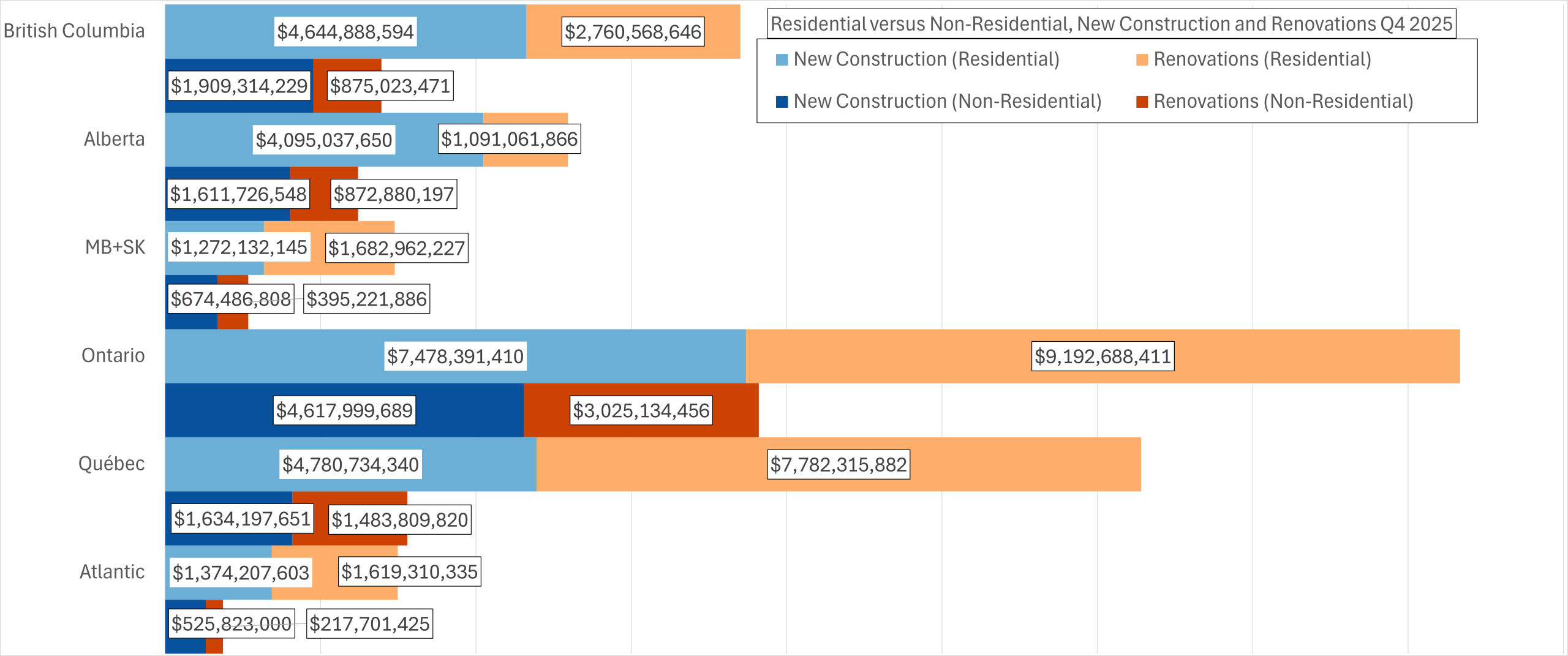

Provincial data reveals that while the national trends hold, the intensity and composition of growth vary significantly by region.

Provincial data reveals that while the national trends hold, the intensity and composition of growth vary significantly by region.

Ontario remains the largest market by a wide margin, but its profile has shifted. Residential new construction declined from $8.6 billion to $7.5 billion, while renovation spending increased sharply from $7.6 billion to $9.2 billion. This mirrors the national trend but at a larger scale. The province continues to rely heavily on reinvestment in existing housing stock, even as new builds slow. Non-residential activity in Ontario remained stable, with new construction edging up slightly and renovation holding near $3.0 billion.

Québec shows one of the most pronounced shifts toward renovation. Residential renovation spending jumped from $4.36 billion to $7.78 billion, a substantial increase that outpaces growth in new construction, which rose more modestly from $4.42 billion to $4.78 billion. This suggests a strong cycle of upgrading and maintaining existing housing. In non-residential segments, however, both new construction and renovation declined, indicating softer demand outside the residential sphere.

British Columbia presents a more balanced growth profile. Residential new construction increased from $4.21 billion to $4.64 billion, while renovation rose from $1.91 billion to $2.76 billion. Both sides of the residential equation are expanding, though renovation is accelerating faster. Non-residential construction also increased slightly, while renovation declined marginally, pointing to stable but selective investment conditions.

Alberta’s data reflects divergence between residential and non-residential dynamics. Residential new construction increased from $3.67 billion to $4.10 billion, but renovation dropped sharply from $1.88 billion to $1.09 billion. This suggests a stronger emphasis on new supply rather than reinvestment. In contrast, non-residential activity grew across both new construction and renovation, indicating broader economic support for commercial and institutional projects.

In the MB+SK region, both residential new construction and renovation increased, with renovation rising more strongly. This aligns with the national renovation trend, though at a smaller scale. Non-residential investment also grew modestly in both categories, suggesting steady, incremental expansion rather than major project-driven swings.

Atlantic Canada remains the smallest market but shows a consistent pattern. Residential new construction increased slightly, while renovation declined modestly, indicating some cooling in reinvestment activity. Non-residential construction increased, but renovation remained relatively flat, pointing to a stable but limited pipeline of projects.

Across provinces, a few patterns emerge. First, renovation growth is widespread but uneven, with Ontario and Québec driving much of the national increase. Second, multi-unit and higher-density markets are supporting new construction in key regions, even as single-family slows. Third, non-residential activity is generally stable, with regional variation tied to local economic conditions and project timing.

The combined effect is a construction landscape that is increasingly defined by adaptation rather than expansion. Investment is flowing toward maintaining, upgrading, and intensifying existing assets, with new construction concentrated in segments and regions where demand remains structurally strong.

Tyler Holt is the Editor of Wood Industry / Le monde du bois magazine. He has a master’s degree in literature and publication, and years of experience in the publishing and digital media industry. His main area of study is the effect of digital technologies on industrial and networked production.

Tyler Holt is the Editor of Wood Industry / Le monde du bois magazine. He has a master’s degree in literature and publication, and years of experience in the publishing and digital media industry. His main area of study is the effect of digital technologies on industrial and networked production.